January 17, 2018

Is Tax-Exemption Necessary? Enlightened Health Systems Should Consider the Unthinkable

In the mid-1800s, English philosopher and political economist John Stuart Mill developed “Utilitarianism,” a framework for making moral decisions. In Mill’s formulation, an action achieves optimal social utility when it advances the well-being of the most people, i.e. “the greatest good for the greatest number.”

No industry is more utilitarian than healthcare. People pursue healthcare careers to alleviate pain and human suffering. It’s not a coincidence that most hospitals operate as Not-for-Profit (NFP), mission-oriented companies.

To support their contributions to social well-being, American society does not require NFP health systems to pay income, sales, excise, property or other taxes. They also can issue lower-cost tax-exempt bonds to finance capital investments. Tax-exemption is not a trivial subsidy. NFP health systems save tens of $billions annually through tax avoidance and lower interest costs.

Not-for-Profit does not mean no profit. NFP health systems are often very large, complex organizations with highly-compensated executives. Ironically, 7 of the 10 most profitable health systems in America operate as not-for-profit companies.

However, tax-exemption is not free. It comes with societal expectations for community benefits exceeding the tax subsidies. By law, NFP health systems must publicly report the level of annual “community benefit” they provide. This mission-benefit discussion between health systems and their communities is becoming increasingly fraught.

The Punching Bag Problem

In July 2017, Politico’s Dan Diamond authored two investigative reports that contrasted the success of America’s leading NFP health systems[1], including Johns Hopkins and the Cleveland Clinic, with the endemic poverty and chronic illness plaguing adjacent neighborhoods.[2]

Apparently being a large employer and providing world-class care isn’t enough. As the Politico articles make clear, society’s implicit social contract with NFP health systems imposes a duty on them to invest substantially in local economic development, workforce empowerment and community health in exchange for tax-exemption benefits.

By contrast, for-profit health systems that pay taxes are free to focus on optimizing resource utilization and profitability. Their community benefit contributions are purely philanthropic and not subject to governmental oversight

A Health Affairs study released in January 2018 confirmed that tax-exempt-hospital investment in community benefit measures increased by only one-half of a percentage point, from 7.6% in 2010 to 8.1% in 2014. Most of that spending went toward unreimbursed treatment, rather than to disease prevention efforts that might improve community health.[3]

Increasingly, tax-exemption is becoming a double-edged sword for NFP health systems. It offers sizable financial benefits, but comes with substantial community benefit obligations. Reflective of the times, challenges to health systems’ tax-exempt status and requests for payments-in-lieu-of-taxes (PILOTs) are increasing.

In post-reform healthcare, all health systems must deliver better outcomes at lower costs to maintain their competitiveness. NFP health systems have the added burden of providing adequate community benefit while transforming their operations. This makes an already tough challenge tougher.

Given the tradeoffs, a utilitarian “greater good” analysis suggests the unthinkable – that select NFP health systems would contribute more to society by paying taxes. This would liberate these organizations to pursue more efficient resource utilization with less public scrutiny. It would enable them to deliver better healthcare at lower costs with enhanced customer service.

Some health systems might consider even going further and converting to for-profit status. This expands capital formation alternatives, but could reduce philanthropic support.

The Downside of Tax-Exempt Status

Tax-exempt status comes with both obvious and hidden burdens. Obvious burdens include defining, delivering and reporting community benefit; withstanding public scrutiny; and managing demands for greater societal contributions. Less obvious burdens include dampened profitability, opaque managerial accountability and sub-optimal governance.

Demands for greater community benefit intensify when profit margins exceed 5%. This implicit profit “cap” hinders organizations from optimizing performance. As a result, NFP health systems tolerate higher levels of inefficiency (i.e., absorb much higher labor costs) than for-profit health systems.

Moreover, NFP boards tend to be large, philanthropically-oriented and non-compensated with diffuse responsibilities and lacking a strategic focus. It’s often difficult for board members to challenge senior management. The result is that many, perhaps most, NFP health systems lack the dynamic board-management tension that drives superior performance.

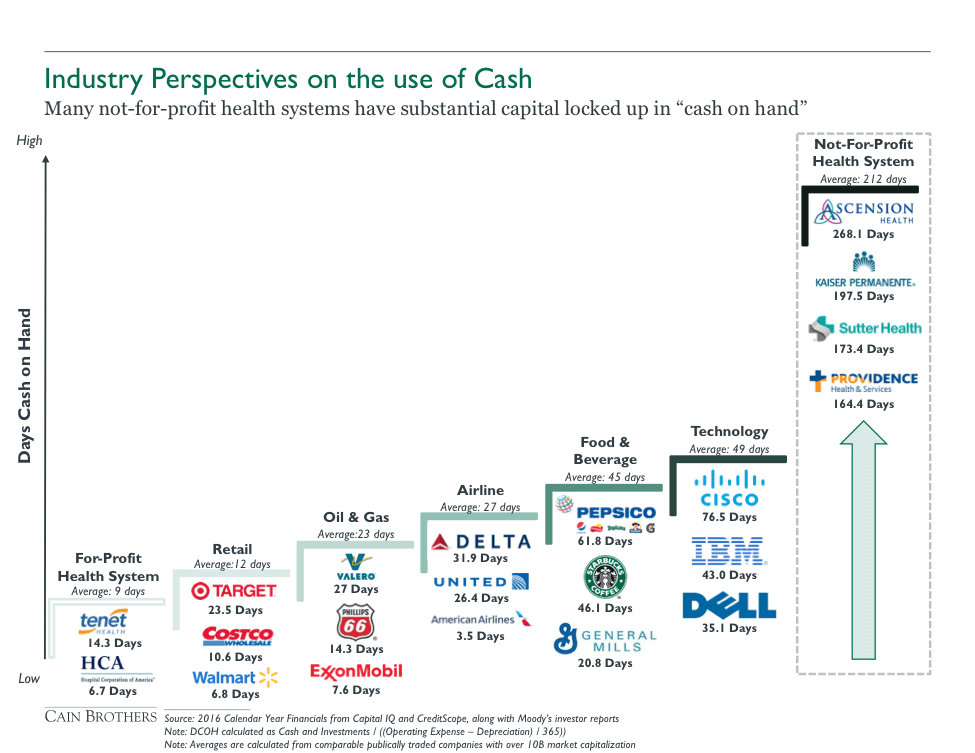

From a capital formation perspective, NFP health systems have fewer options for making capital investments than their for-profit counterparts, adding to the costs of their tax-exempt status. NFP health systems can only fund capital from organizational cash flow, debt, asset sales, cash reserves and philanthropy. Their not-for-profit status excludes them from participating in equity-based funding alternatives, such as stock issuance.

Given limited capital formation alternatives, NFP health systems must maintain high cash levels to access publically-traded debt markets. Keeping cash on the balance sheet rather than investing for “highest and best uses” results in sub-optimal resource utilization and a significant “opportunity cost.”

For-profit health systems can apply taxable debt and private equity investment to create more efficient capital structures. For-profit health systems also have greater flexibility in structuring debt offerings (e.g. senior, secured, junior, unsecured debt structures) to optimize relationships between debt costs and pledged assets. By contrast, tax-exempt bonds have uniform security provisions, limited structuring flexibility, significant “use” limitations on debt proceeds and higher compliance costs.

Relative to NFP health systems, for-profit systems enjoy less stringent debt covenants, tax-deductible interest payments and more “liquid” debt markets that support efficient debt pricing. Greater liquidity, structuring flexibility and no “use” limitations offset the lower interest rates in the tax-exempt debt markets. For these reasons, taxable debt offerings by NFP health systems have increased significantly in the last ten years.

Does Tax-Exemption Matter?

NFP hospitals constitute the majority of America’s hospitals. 2,849 of 5,534 registered U.S. hospitals are non-governmental not-for-profit entities[4], including healthcare’s most prestigious brands, such as Mayo Clinic and Mass General Hospital.

Prior to World War I, charities and religious organizations funded most NFP hospitals through research and education grants. Hospitals were largely warehouses for the very sick, and primarily served the indigent.

These operating and funding patterns changed as hospital care improved, health insurance emerged, payment for healthcare services institutionalized and hospitals merged into health systems. “Charity” hospitals gradually disappeared while charitable care became exempt from federal tax law after 1913.[5]

In the modern era, maintaining tax-exempt status requires that NFP health systems provide broad access to healthcare services and generate social benefit for their communities. Activities that benefit communities include health education, charitable healthcare services, health screenings, medical research and medical education.

Designed to increase access to healthcare services, the Affordable Care Act (ACA) has increased hospital revenues and decreased their need to provide “charity care.” Between 2013 and 2015, revenues for the top 7 U.S. News hospitals increased 15% from $29.4B to $33.9B. During the same period, charity care spending at these hospitals dropped 35% from $414M to $272M, less than 1% of revenues. Meanwhile, hospital profit margins hit a record 8.3% in 2014.[6]

Subsequent political uncertainty around the ACA compounds the community-benefit conundrum. The repeal of the individual mandate is likely to increase the need for charitable care as fewer Americans elect to pay for insurance coverage. However, NFP hospitals may have less revenue going forward.[7]

When it comes to business operations, for-profit and not-for-profit health systems are quite similar. As Harvard professor Clayton Christensen has noted in public forums, both for-profit and NFP hospitals provide the same services, comply with the same governmental regulations and must generate profits to guarantee their long-term sustainability.

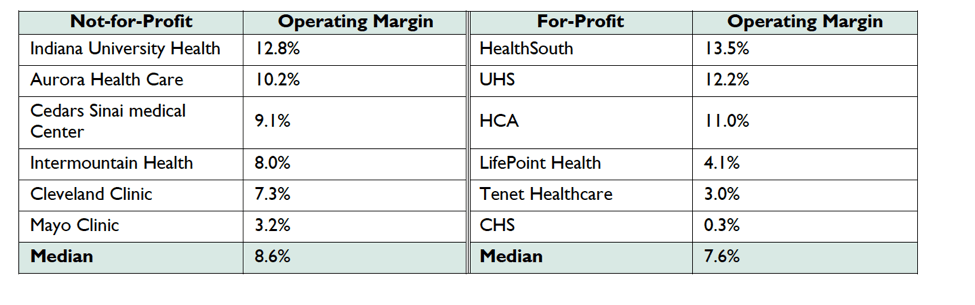

For-profit, tax-paying hospitals provide equivalent levels of charity care as NFP hospitals, and NFP health systems generate equivalent operating margins to their for-profit counterparts (see chart above).[8] When asked, most Americans cannot identify whether their local hospital is taxable or tax-exempt.

To date, NFP hospitals have expertly deflected demands that they offer more expansive, explicit and transparent benefits to their communities in exchange for not paying taxes and accessing tax-exempt debt.

The ACA requires NFP hospitals to conduct health needs assessments and pursue community health improvement. The law did not, however, specify measurable indicators to assess compliance.

Longer term, the inability to distinguish tax-exempt and taxable care delivery poses an existential challenge for NFP health systems. It makes justifying NFP hospitals’ preferential tax status increasingly difficult.

“Unlocking” the Balance Sheet through For-Profit Conversions

By converting to for-profit status, health systems may choose to redirect sizable cash assets to “higher and better” uses. For-example, a newly-converted health system can transfer “unlocked” cash into not-for-profit foundations that provide the following types of targeted services:

- Tackling social determinants of health

- Improving local food quality

- Investing in local pharmacies

- Eliminating lead in drinking water

- Improving local infrastructure

- Investing in education and engagement programs

More importantly, by converting to for-profit status, health systems can reorient operating profiles to become more competitive. Steward Health Care pursued this strategy to achieve significant operational and financial agility while revitalizing its care mission.

In 2010, Caritas Christi was a failing Massachusetts-based system with six hospitals, sub-standard facilities, declining patient volume, poor quality scores and substantial operating losses.

Lacking alternatives, Caritas Christi sold its assets to Cerberus, a private equity company, rebranded itself as Steward Health Care and embarked on a path to profitability, transformation and national significance.

Steward restructured its debt, invested in new capital projects, expanded to 9 hospitals and embraced Accountable Care. With its acquisition of 8 Community Health Systems hospitals in May 2017 and 19 Iasis hospitals in September 2017, Steward became a 36-hospital system operating in 10 states with approximately $8 billion in annual revenues.[9]

Today Steward operates as a risk-bearing accountable care company well-positioned for continued growth and profitability. Physician-led and customer-focused, Steward demonstrates that for-profit health systems can break free of volume-base business practices to deliver high-quality, cost-effective care while benefiting local communities with tax dollars, economic growth and improved population health.

Ends and Means

Ultimately, organizational tax status is a tactical decision. The true measures of hospital performance are quality and consistency of care outcomes, operational efficiency and superior customer experience.

Paying taxes would not require hospitals to forego their non-profit status, but it would relieve them of filing community benefit reports and free them to operate with greater strategic flexibility and without artificially-imposed profitability constraints. These could turn out to be competitive advantages as the healthcare marketplace becomes more competitive, transparent and consumer-oriented.

Debating community benefit can become a distraction that compromises health systems’ ability to optimize performance. Converting to for-profit status will be the right strategy for some health systems, like Steward Health Care, that want to reposition and/or redirect cash assets to more beneficial purposes.

In the final analysis, it’s not whether hospitals pay taxes that will determine their long-term sustainability and benefit to society. It’s whether they can deliver the right care at the right time in the right place at the right price.

[1] http://www.politico.com/interactives/2017/obamacare-non-profit-hospital-taxes

[2] http://www.politico.com/interactives/2017/obamacare-cleveland-clinic-non-profit-hospital-taxes/

[3] https://www.healthaffairs.org/doi/abs/10.1377/hlthaff.2017.1028?journalCode=hlthaff

[4] http://www.aha.org/research/rc/stat-studies/fast-facts.shtml

[5] http://scholarship.law.edu/cgi/viewcontent.cgi?article=1116&context=jchlp

[6] http://www.politico.com/interactives/2017/obamacare-non-profit-hospital-taxes/

[7] https://khn.org/news/despite-prod-by-aca-tax-exempt-hospitals-slow-to-expand-community-benefits/

[8] http://www.politico.com/interactives/2017/obamacare-non-profit-hospital-taxes/

[9] https://www.prnewswire.com/news-releases/steward-health-completes-acquisition-of-iasis-healthcare-300528426.html

CO-AUTHOR

David Morlock

David Morlock is a senior banker in the Firm’s Health Systems M&A Group. Mr. Morlock joined Cain Brothers in 2016 with 30 years of experience as a health system executive. His track record includes strategy development, mergers and acquisitions, affiliation agreements, joint ventures, major capital investments, and other unique arrangements tailored to meet the needs of healthcare organizations’ specific circumstances. Notable and innovative transactions and advisory engagements include the divestiture of MDwise health plan by Indiana University Health, acquisition of Ohio Valley Health by Alecto, affiliation between ProMedica and the University of Toledo College of Medicine, the University of Michigan Health System sale of M-Care to Blue Cross Blue Shield of Michigan, and the University of Michigan’s acquisition of a major research campus from Pfizer. Mr. Morlock is a frequent author of articles and speaker on health care industry mergers and acquisitions and strategic capital insights. Mr. Morlock earned an MBA from Eastern Michigan University’s Owen School of Business and is an honors graduate of Slippery Rock University.

David Morlock is a senior banker in the Firm’s Health Systems M&A Group. Mr. Morlock joined Cain Brothers in 2016 with 30 years of experience as a health system executive. His track record includes strategy development, mergers and acquisitions, affiliation agreements, joint ventures, major capital investments, and other unique arrangements tailored to meet the needs of healthcare organizations’ specific circumstances. Notable and innovative transactions and advisory engagements include the divestiture of MDwise health plan by Indiana University Health, acquisition of Ohio Valley Health by Alecto, affiliation between ProMedica and the University of Toledo College of Medicine, the University of Michigan Health System sale of M-Care to Blue Cross Blue Shield of Michigan, and the University of Michigan’s acquisition of a major research campus from Pfizer. Mr. Morlock is a frequent author of articles and speaker on health care industry mergers and acquisitions and strategic capital insights. Mr. Morlock earned an MBA from Eastern Michigan University’s Owen School of Business and is an honors graduate of Slippery Rock University.

Disclaimer:

The information contained in this report was obtained from various sources that we believe to be reliable, but we do not guarantee its accuracy or completeness. Additional information is available upon request. The information and opinions contained in this report speak only as of the date of this report and are subject to change without notice. This report has been prepared and circulated for general information only and presents the authors’ views of general market and economic conditions and specific industries and/or sectors. This report is not intended to and does not provide a recommendation with respect to any security. Any discussion of particular topics is not meant to be comprehensive and may be subject to change. This report does not take into account the financial position or particular needs or investment objectives of any individual or entity. The investment strategies, if any, discussed in this report may not be suitable for all investors. This report does not constitute an offer, or a solicitation of an offer to buy or sell any securities or other financial instruments, including any securities mentioned in this report. Nothing in this report constitutes or should be construed to be accounting, tax, investment or legal advice. Neither this report, nor any portions thereof, may be reproduced or redistributed by any person for any purpose without the written consent of Cain Brothers.

Cain Brothers is a member of SIPC. © 2016 Cain Brothers and Company, LLC

About the Authors

Recent Posts