February 25, 2026

Who’s Winning the Alternative Payment Model Race?

I spent most of my space in last week’s blog post thanking AHIP for saving the annual progress report on alternative payment model (APM) adoption from the clutches of the Centers for Medicare and Medicaid Services (CMS) and the Make America Healthy Again movement. I spent the balance of the post on some interesting data from the report on how much money still flows from payers to providers via traditional fee-for-service reimbursement contracts.

I’m going to pick up where I left off because I ran out of room to tell the entire story.

AHIP’s APM Measurement Effort report is based on an analysis of claims data from commercial health plans, traditional Medicare, Medicare Advantage (MA) plans and state Medicaid programs. The analysis determines how much money those four payers pay to providers through four escalating categories of APMs with traditional fee-for-service models with no link to quality or value on the low end (Category 1) and four variations of population-based payment models on the high end (Category 4).

The framework considers the four variations of population-based models in Category 4 and the three variations of APMs built on a fee-for-service architecture in Category 3 as value-based payment models.

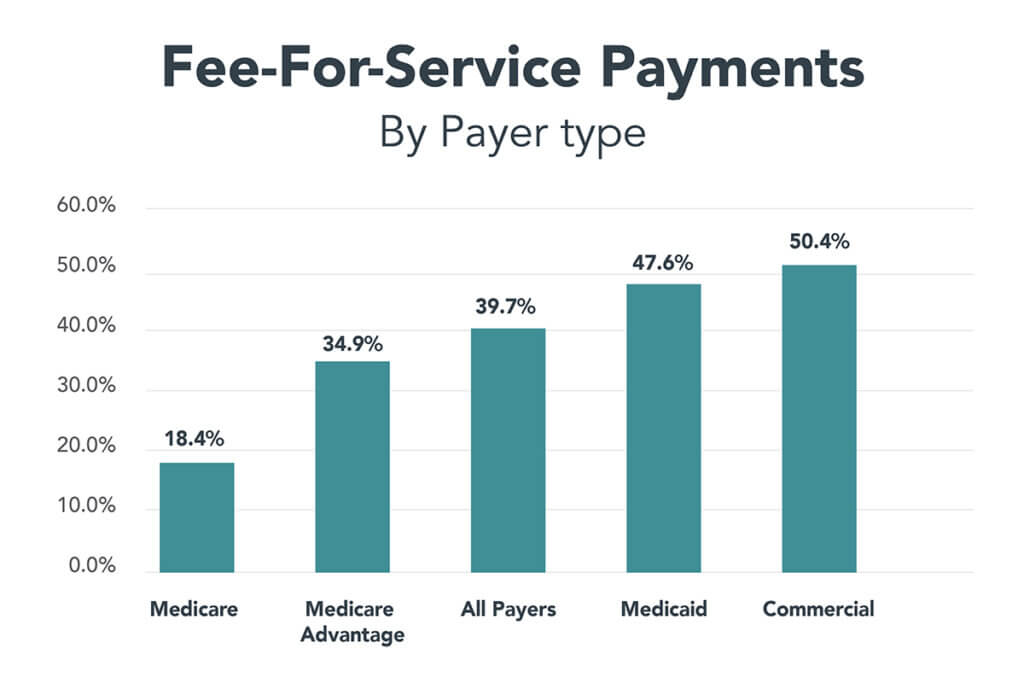

The chart below shows you how much money the four payers paid providers in 2024 through Category 1, or traditional fee-for-service models with no link to quality or value:

Source: APM Measurement Effort Report

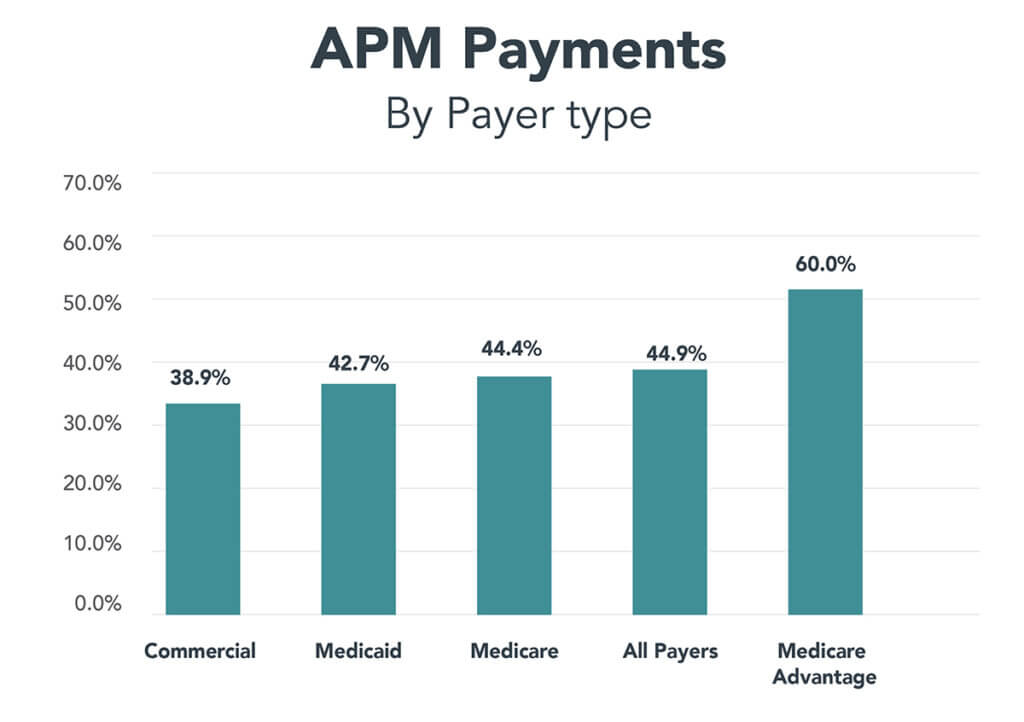

Meanwhile, this chart shows you how much money the four payers paid providers in 2024 through seven variations of APMs in categories 3 and 4:

Source: APM Measurement Effort Report

Conventional wisdom says: As Medicare goes, so go commercial health insurers. In other words, Medicare is such a dominant payer in the healthcare system — where it goes, others will follow.

What the new report’s analysis and the above charts show is that’s not true when it comes to APMs. Where Medicare goes, commercial health plans go the other way. Or, where Medicare goes, commercial health plans struggle to keep pace. Or, traditional Medicare and Medicare Advantage have the market leverage over providers to institute whatever payment models they want while commercial health plans do not.

There are lots of good healthcare market storylines here waiting for some young enterprising healthcare business reporters to pursue. I’m just turning on the light.

It’s time to build a better healthcare system that pays providers based on outcomes, not volume.

Thanks for reading.

About the Author

Recent Posts