December 15, 2015

Rational Lending: Demystifying Medical Student Loan Debt

Market Corner Commentary—Demystifying Medical Student Loan Debt, for December 16, 2015

Winston Churchill famously observed that “Russia was a riddle wrapped in mystery inside an enigma.” Churchill’s language provides an apt description for medical student loans in America today. Loan programs designed to help students pay for medical education are complex, expensive and shrouded in misunderstanding.

U.S. Federal student loan debt is massive, exceeding $1.1 trillion – far greater than either credit card debt ($793 billion) or auto debt ($839 billion). The amount of student debt has quadrupled since 2000 while the number of borrowers has more than doubled to 42 million. Default rates are at a twenty-year high.[1]

The Confusing World of Medical Student Loan Debt

Within the universe of student loan debt, medical debt is a small but golden nugget. Default rates are low. Medical professionals earn good incomes and market demand for their services is exceptionally strong.

At the same time, medical education costs are skyrocketing. Medical professionals, particularly doctors, assume mammoth levels of debt to finance their educations. The AAMC reports median debt for graduating doctors in 2014 was $180,000.[2] The average student loan debt for medical school has more than doubled in the last fifteen years.[3]

Loan payment forbearance during medical school and residency compounds the debt burden. The numbers can be scary. In 2013, Federal Reserve Chairman Ben Bernanke testified before Congress that his son’s student loan debt would exceed $400,000 upon graduation from Weil Cornell Medical College in New York City.[4]

Forty percent of medical school graduates plan to pursue publically-funded loan forgiveness/repayment programs. These programs can offer significant debt relief, but come with stipulations, limitations and risk of punitive retroactive adjustment.

Private restructuring alternatives offer medical professionals significant debt payment relief with less risk and greater flexibility than government-sponsored programs. These benefits expand when health system employers subsidize debt restructuring programs.

Large debt burdens, escalating costs, multiple debt relief programs and a changing medical delivery environment amplifies risks for both medical professionals and their employers. The healthcare industry requires a rational diagnosis of the medical debt “disease” and prescriptions for its “cure”.

Big Picture: Student Loan Defaults Concentrated in Non-Traditional Borrowers

The massive increase in student loan debt and its corollary societal costs reflect a broader contagion afflicting higher education as more students pursue advanced education, the costs of higher education soar, schools exploit Federal student loan programs and post-industrial workforce skill requirements elevate.

A September 2015 Brookings research paper finds student loan defaults concentrate in “non-traditional” borrowers – enrollees in for-profit schools and community colleges with low completion rates. An inability to find adequate employment after leaving school lead disproportionate numbers of these non-traditional borrowers to default on their student loans.

In 2011, non-traditional borrowers accounted for 70 percent of student loan defaults. Overall 21% of non-traditional borrowers default within two years of leaving school.

By contrast, only 8 percent of four-year college attendees and only 2% of graduate students default on their student loans within two years of leaving school. Moreover, student borrowers with higher debt levels achieve higher earning levels upon graduation. In aggregate, these borrowers correlate their level of educational debt with expected earnings.

Traditional Borrowers Repay Their Loans, But Want Relief

The good news is that traditional borrowers, particularly graduate students, constitute a strong credit pool and are well-positioned to benefit from private, market-based debt restructuring programs. Market-based restructuring alternatives are not burdened by the costs and complexity infecting governmental restructuring programs.

Moreover, private lenders can work with employers to magnify the benefits of student loan restructuring through employee benefit programs. Young professionals strongly favor these types of programs. Employers take note.

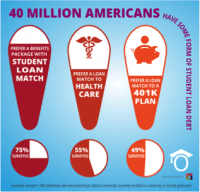

A recent survey by Iontuition of individuals with student loans found the following: 75% favor employer matches for student loan payments; 55% prefer having health benefit contributions applied to student loan debt; and 49% want employers to fund student loan repayment more than 401K contributions.

Why Government Isn’t Here to Help

Governments exist to homogenize risk and distribute mitigation costs. All Americans benefit from national defense. Some pay more for this benefit than others. Policy debates center on which risks to homogenize and the mechanisms for funding risk mitigation.

The U.S. government supports higher education through grants, subsidies and loan programs. As discussed above, the rise of for-profit schools largely funded by student loans for non-traditional borrowers has led to high default levels and substantial losses. Offsetting support for higher education is the need for student loan programs to be solvent. Recent Congressional and administrative action has supported solvency over program expansion. Two policy realities underpin the government’s current approach:

- The Department of Education now operates higher education support programs on a self-sustaining basis. The 2014 Congressional Budget Office (CBO) forecasts the Department of Education will net $127 billion in “negative subsidies” over the next ten years.”[5] In CBO-speak, “negative subsidies” means “profit.”

- The Department of Education covers loan defaults, funds subsidies and generates surpluses by charging substantially higher interest rates than the Department’s funding cost. In essence, students repaying their loans also pay the costs of defaulting student loans, grants, subsidies and loan forgiveness programs.

The Federal government has taken the following two steps toward making the student loan programs self-sustaining:

- It’s tightened regulation of student loans to for-profit schools and community colleges. Since 2011, loans to for-profit schools have dropped 44% and loans to community colleges have dropped 19%[6]

- Congress passed legislation in 2013 that requires the Department of Education to charge market-based interest rates for student loans. Initially this provision has lowered borrowing rates, reflecting exceptionally low current interest rates. As short and long-term rates rise, student loan interest rates also will rise.

The political debate continues. Senator Elizabeth Warren is advocating legislation that will make student loans lower-cost and more accessible. Others advocate tightening eligibility for subsidy and loan-forgiveness programs. Tighter eligibility for loan-forgiveness programs would have a disproportionate impact on medical professionals.

Private Market Solutions

In well-functioning markets, companies emerge to “solve problems” for customers. The “fittest” companies meet customer needs and adapt to customer preferences. These companies understand they exist solely to provide “value” to customers.

The Department of Education relies on a wide 2%-5% “spread or float” between its funding costs and the unsubsidized loan rates it charges students to generate surpluses. The Department uses these surpluses to offset default costs, recapitalize its loan portfolio and fund subsidies/loan forgiveness. The high interest rates on unsubsidized loans create refinancing opportunities for private companies. Given their heavy debt positions, medical professionals can benefit enormously from private refinancing alternatives

Lending Case Study

The founders of LinkCapital recognized a market need among medical professionals for cost-effective student loan debt restructuring. Their business-to-consumer service model offers transparent, flexible, user-friendly programs tailored to individual borrower needs and preferences. Their programs can lower interest costs by more than 3% and save thousands. Link understands that customers must “win” for the company to prosper.

Link strives to enhance its products by partnering with health systems in a business-to-business service model. In order to attract and retain medical professionals, many health systems subsidize education costs and/or provide stipends to offset student loan costs. By working with Link, health systems improve the efficiency, marketability and effectiveness of their investments in workforce education – a “win-win-win” formula.

Bottom-up, market-driven solutions are always superior to unsubsidized governmental solutions. Private companies target specific client segments, understand their needs and deliver services that meet those needs. Top-down government programs must balance multiple interests and carry high administrative costs. By necessity, governments prefer one-size-fits-all program solutions.

Restructuring high-cost medical student loan debt is a classic example of private market “solutions” addressing profound customer needs. Companies like LinkCapital improve the lives of medical professionals with every dollar they save.

A version of this article appeared in “Becker’s Hospital Review” on December 7, 2015. Please note the author serves on the Link Capital Advisory Board.

[1] Source: Brookings, A crisis in student loans? How changes in the characteristics of borrowers and the institutions they attended contributed to rising loan defaults, Adam Looney and Constantine Yannelis, September 2015

[2] AAMC Debt, Costs and Loan Repayment Fact Card, October 2014

[3] Source: AAMC Analysis in Brief, Volume 12, Number 2, July 2012

[4] “Medical School at $278,000 Means Even Bernanke Son Has Debt”, Bloomberg Business, Janet Lorin, April 11, 2013

[5] Emily DuRoy, fusion.net, “Student Loan Borrowers Mean Big Money for the Government”, April 16, 2014

[6] Brookings Report

About the Author

Recent Posts